Changing Landscapes of Banking Sector

By BYJU'S Exam Prep

Updated on: September 25th, 2023

The banking sector needs to grow at a higher rate than the GDP growth rate in order to ensure that our growth momentum continues. However, whether the banking industry can live up to such expectations, is debatable.

The banking sector is undergoing a number of changes in terms of asset quality, technology and regulations.

The sector’s success in adapting to these changes will determine whether our banks will remain the main source of financing India’s economic activities or will undergo a gradual change in their roles and functions.

CHANGING LANDSCAPES OF BANKING SECTOR

Is it a more financially included India that is being thought about or is it a ‘digital’ or ‘connected’ India that is new? It is a bit of all and beyond. There are seven key themes which would define the Indian economy and Indian banking sector in the days to come.

These are:

- Demography

- Urbanization

- Digitization

- Industrialization

- Education

- Financial Inclusion and

- Global integration

In the growth trajectory of the financial services, the digital revolution promises extraordinary gains in the productivity of the banking industry, unprecedented improvements in the quality of customer experience and a fundamental shift in the nature and intensity of the competition.

If we make an excursion into the post-demonetization arena of the Indian economy, we feel that financial services are more digitally advanced than many industries.

POSITIVES – CHANGING LANDSCAPES

1. Demography: Much has been talked about the demographic dividend that India possesses. On the one hand, the numbers present a sustained opportunity for the banks in terms of a new stream of customers.

2. Urbanisation: India is also witnessing a growing trend of urbanization, this would open up huge business opportunities for the banks for the creation of public infrastructure, housing, consumption, education needs of customers and so on.

3. Digitization: Digitization is another area which is being pursued relentlessly by the Government. There is a massive focus on enhancing internet penetration in the country.

- As the number of internet users in the country grows, the banks would be able to better utilize this medium as a delivery channel and as an opportunity to be tapped.

- Digital Revolution comes in India on 6th July 2016 when the government launched its UPI (Unified Payment Interface).

- Digital banking is the incorporation of new and developing technologies throughout a financial services entity, in concert with associated changes in internal and external corporate and personal relationships.

Current Digitisation Platforms & Trends

- Bharat QR Code

- Unified Payments Interface (UPI )

- Bharat Interface for Money (BHIM )

- National Unified USSD Platform (NUUP)

- Aadhar Enabled Payment System (AEPS)

- Rupay Card

- Mobile Commerce

Upcoming Digitisation Trends

- Using of Big Data, AI and advance analytics.

- Exploring advanced Technologies (IoT, voice)

- Using of Blockchain Technology

- Open APIs

4. Industrialization: The Government’s ‘Make in India’ pitch also touches the right cords and efforts to increase the stagnant share of manufacturing in GDP. If that materializes, it would mean adding more domestic jobs and attendant corporate and retail business opportunities.

5. Education: Likewise, there is a tremendous scope for improving the level of education in the country with a strategic focus on the four Es i.e. Expansion, Equity and Inclusion, Excellence & Employability. It would entail significant changes in consumer awareness, needs, demands, and expectations.

6. Financial Inclusion: Financial inclusion is the pursuit of making financial services accessible at affordable costs to all individuals and businesses. Financial inclusion strives to address and proffer solutions to the constraints that exclude people from participating in the financial sector.

Following are the initiatives towards Financial Inclusion :

- Lead Banking

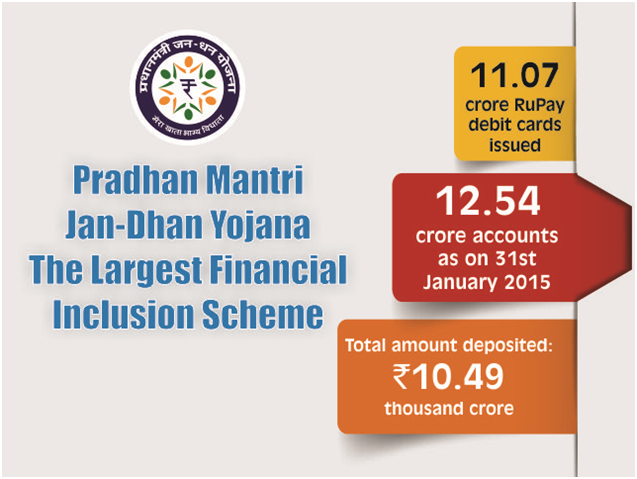

- Pradhan Mantri Jan Dhan Yojna (PMJDY)

- Payments & Small Finance Banks.

- Basic Savings Bank Deposit Account ( BSBDA )

7. Global Integration: Growing global integration, which is already having significant repercussions on the financial sector. Be it the quantitative easing by the advanced economies and the subsequent withdrawal of it, convertibility of currency, making or breaking of a regional alliance of economies and currencies etc. There could be other hitherto unforeseen developments affecting the global structure of finance.

FINANCIAL TECHNOLOGY

The asset quality issue of banks will get addressed in due course. However, it will be the pace of technological advancement that will test the banking industry more. During the last 2-3 years, use of technology has become integral to banking operations and technology is used for data analysis, for understanding the credit needs of customers, customer interaction, etc. and even helps banks to offer more focused products to customers. Thus, banking and technology are now inseparable.

CROWD-FUNDING

Another phenomenon which is still at a nascent stage in India but has the potential to emerge as a competition, as well as a disruption to traditional banking, is crowd-funding.

- Presently, the crowdfunding of projects is done online on social network platforms and these mostly bypass traditional banking intermediaries. Crowdfunding is an attractive route especially for MSMEs and start-ups whom banks are reluctant to fund.

- Given that one of the core concepts of crowdfunding is the focus on transparency, global banks are adapting their business models in order to follow suit and provide more transparent products.

- Before it emerges as a competitor, Indian banks can consider setting up digital platforms to bring together potential borrowers and lenders to promote and finance entrepreneurs.

- This would be one way of benefiting from the “collective intelligence” of the crowd. However, RBI would need to put in place necessary regulations for that to happen.

CHALLENGES / NEGATIVES – CHANGING LANDSCAPES

(1) Digital Banking shortcomings: Realizing the potential of digital banking is easier said than done with legacy challenges because of the incumbency and conventional mental models, existing technology and operating platforms.

- As the adoption and acceptance of more and more payment methods increases, necessary measures to prevent and detect fraud and risk should be in place with every new method.

- India is at a crucial stage where the government, banks, service providers and consumers themselves are working towards a less-cash economy.

- It is important that consumers place their faith in the payments system and are not deceived. Preempting security threats and ensuring consumer financial safety should be an important part of this new payment trends.

The problem of stressed assets

The Indian banking sector has been in the news ever since the Asset Quality Review was introduced in 2015. The review brought to the fore a significant amount of stress in the banking system, especially in the public sector banks (PSBs).

- The asset quality has been on a declining trajectory as per the Financial Stability Report (FSR) released by RBI. In addition, banks are capital starved. It has been seen that Indian banks need a capital infusion to meet the Basel-III norms.

- Also, the definition of NPAs is probably worth reviewing. It does not make logical sense to have the same yardstick for NPA classification as for a car loan, a home loan and or an infrastructure loan. The risks associated with each asset class are different from the others and by that logic, the definition of NPAs should also vary asset-wise.

- Indian banks’ emphasis and focus on security rather than the projected cash flows while doing credit assessments and loan appraisals are quite intriguing. Going forward, cash flows should get adequate weightage in lending decisions.

IMPACT OF NEW BANKING LANDSCAPE ON THIS SECTOR

The new banking landscape would impact the processes currently in vogue in the sector.

(1) Competition and Consolidation: Competition and consolidation in the sector is an impending development that the banks would have to contend with sooner rather than later.

- New banks such as small finance banks and payments banks might mark their presence, There could be consolidation and mergers between the existing market players.

- No doubt there is plenty of opportunity for the well organized and mainstream regulated players to wean away the customers from unregulated shadow banking entities. But, the existing players can afford to stay in denial at their own peril.

- We have seen competition giving a tough run to the monopoly players.

- RBI has already started the “on tap” bank licensing process for introducing more varieties of differentiated banks. Also, there is a healthy appetite from the foreign banks to enter this country.

(2) Risk Management: Risk Management in banks is of the same vintage as the banks themselves. The banks are in the business of taking risks and hence they need to have a risk management framework in place.

- It has been pursued in our banking system more under compliance compulsions and has not been dovetailed in the banks’ businesses processes as much as they ought to have been.

- As the complexity in the financial world grows, the banks would need to carefully consider and set their risk appetite after duly evaluating their capital level as also the skillsets of the officials entrusted with the management of risks.

CONCLUSION

- Most retail banks have taken important steps in omnichannel and other digital capabilities. However, in such a competitive climate, success may well be determined by the one who fully integrates analytics, personalized anywhere-anytime advice, and other digital proficiency.

- Under the circumstances, it would be important for the banks to keep track of emerging trends and be prepared not only to negotiate through the imminent challenges but simultaneously be ready to latch on to the opportunities that present themselves.

- Also, there is a need for a new thought leadership not only at the bank management level but at the regulator level too.

- Technology is continuously evolving and the contours of the banking sector are also changing. There is a need to upgrade the skill-sets.

Thanks

Team Gradeup