Management Accounting Study Notes

By BYJU'S Exam Prep

Updated on: September 11th, 2023

Management Accounting Study Notes – According to The American Institute of Certified Public Accounts (AICPA), accounting is ‘an art of recording, classifying and summarizing in a significant manner and in terms of money, transactions and events which are, in part at least, of a financial character, and interpreting the results thereof”.

- A service activity

- A descriptive/analytical discipline

- An information system

Bookkeeping is not accounting, but it is only an activity concerning the recording of financial data.

Key Subfields of Accounts

- Financial Accounting

- Cost Accounting

- Management Accounting: Reporting and decision making

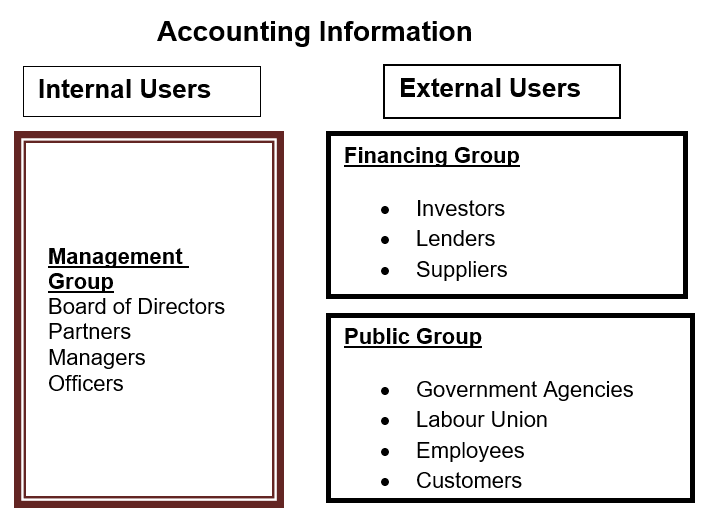

Users of Accounting Information

- Investors

- Lenders

- Suppliers

- Customers

- Government agencies

- The public and

- Employees

Click here to download the PDF

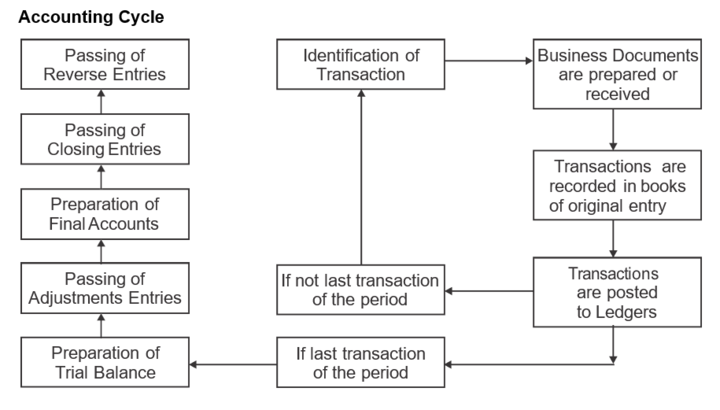

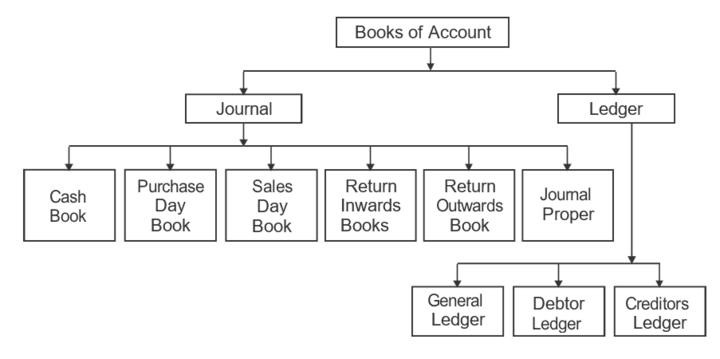

Accounting Cycle, Journal & Ledger Accounting Cycle

| BBA Entrance Exams | |

| SET BBA | IPMAT |

| GGSIPU CET | JIPMAT |

| DU JAT | UGAT |

| NPAT | NCHMCT JEE |

Recording of Transactions in Journal

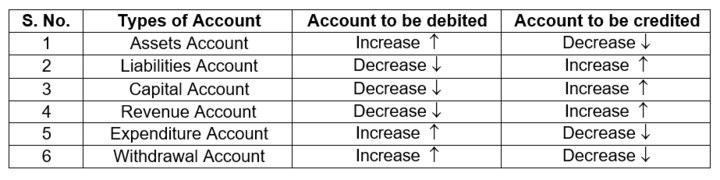

Double Entry System: The rules of the double-entry system can be explained in terms of the basic accounting equation.

Liabilities + Capital = Assets

Rules for Debit and Credit (Traditional)

1- Personal Accounts: Debit The Receiver, Credit The Giver

For example, When Prem gives a loan to the business, the Bank account (receiver) is debited and the Prem account (Giver) is credited.

2- Real Accounts: Debit What Comes In, Credit What Goes Out.

For example, When a car is purchased for cash, the car account is debited (as it comes into the business) and the cash account is credited (as it goes out of the business).

3- Nominal Account: Debit All Expenses And Losses, Credit All Incomes And Gains.

For example, When salary is paid, the salary account is debited ( as it is an expense) and the cash account is credited (as the asset is going out).

4- Valuation Account: Debit the account when the account is to be reduced and credit the account when the account is to be increased. Valuation Accounts are usually balance sheet accounts used with any other balance sheet account to record a carrying amount of an asset or liability. Example, Allowance for Doubtful Accounts, Accumulated Depreciation etc.

Classification of Account

Accounting Concepts, Bases and Policies

Accounting Concepts: These assumptions are rules of the game and they have emerged from consensus.

- Money Measurement Concept: Money has been adopted by the accounting system as its basic unit of measurement.

- Dual Aspect Concept: There is always two-sided impact. Assets = Liabilities + Capital.

- Going concern concept: Accounting is based on the assumption that the accounting unit is to remain in operation into the foreseeable future in pursuit of its goals and objectives.

- Periodicity Concept: Accounts will be prepared at regular intervals.

- Accrual Concept: The accrual concept is an accounting system that recognizes revenues and expenses as they are earned or incurred respectively, without regard to the date of receipt of payment.

- Matching Concept: Since the matching concept is an essential part of accrual accounting, these two are often used interchangeably. Like the accrual concept, the matching concept also results from the periodicity concept. The matching concept requires that the expenses for an accounting period should be matched against related incomes, rather than recognizing revenues as being earned at the time when cash is received or recognizing expenses when cash is paid, and thereby, comparing cash receipts with cash payments.

- Realization Concept: Revenue should only be brought into account when it is actually realized.

- Materiality Concept: Materiality implies significance, substance, importance and consequence. The materiality concept permits other concepts to be ignored if the effects are not considered material. The concept of materiality is the threshold for recognition of a transaction in the accounting process.

- Consistency Concept: Follow the same system for the long term. The consistency concept relates to the method of measurement in accounting.

- Conservatism (or prudence) Concept: Prior recognition of Losses. Where there is a reasonable choice of accounting treatments, the concept of conservatism refers to early recognition of unfavourable events. ‘Recognize all losses and anticipate no gains’.

- Historical Cost Concept: Record at acquisition cost.

Capital and Revenue

- Capital expenditure is the outflow of funds to acquire an asset that will keep on the benefit of the business for more than one accounting period.

- Revenue expenditure is the outflow of funds in order to meet the day to day or short term expenses of a business. These expenses will benefit the firm for the current period only. Revenue expenditures are incurred to manage the daily business and to maintain the good condition of capital assets.

Some examples of capital expenditure:

(1) Purchase of land, building, machinery or furniture.

(2) Cost of leasehold land and building.

(3) Cost of purchased goodwill.

(4) Preliminary expenditures.

(5) Cost of additions / extensions to existing assets.

(6) Cost of overhauling second-hand machines.

(7) Expenditure on putting the asset into working condition.

(8) The cost incurred for increasing the earning capacity of a business.

Some examples of revenue expenditure:

(1) Salaries and wages paid to the employees.

(2) Rent and rates for the factory or office premises.

(3) Depreciation on plant and machinery.

(4) Consumable stores.

(5) Inventory of raw materials, work-in-progress and finished goods.

(6) Insurance premium.

(7) Taxes and legal expenses.

(8) Miscellaneous expenditure

===========================