- Home/

- GATE MECHANICAL/

- GATE ME/

- Article

Cost Estimation Study Notes for Chemical Engineering

By BYJU'S Exam Prep

Updated on: September 25th, 2023

As a chemical engineer, understanding and accurately estimating project costs are crucial skills. These study notes are specifically designed to equip you with the knowledge and techniques needed to perform effective cost estimation in the field of chemical engineering. Cost Estimation Study Notes for Chemical Engineering provide a comprehensive overview of various cost estimation methods and strategies.

Whether you are involved in process design, plant construction, or project management, having a solid understanding of cost estimation is essential for successful project execution. With these study notes, you will delve into topics such as equipment costs, labour expenses, material costs, and indirect costs, enabling you to make informed decisions and ensure efficient financial planning throughout the project lifecycle. By mastering the principles and techniques covered in these study notes, you will enhance your abilities as a chemical engineer and contribute to the overall success of your projects.

Check Out: Customized study planner including topics prioritization and time management

Table of content

Cost Estimation

The purpose of cost estimation is to forecast the cost of a project prior to its actual construction. Cost estimating is a method of approximating the probable cost of a project before its construction. The exact cost of a project is known after the completion of the project. The cost estimate is prepared at various stages during the life of a project on the basis of the information available during the time of preparation of the estimate.

Capital Investments

The capital needed to supply the necessary manufacturing and plant facilities is called the fixed-capital investment, while that necessary for the operation of the plant is termed the working capital. The sum of the fixed-capital investment and the working capital is known as the total capital investment.

Check Out: Career Opportunites Through GATE

Fixed-Capital Investment

The fixed-capital portion may be further subdivided into manufacturing fixed-capital investment and nonmanufacturing fixed-capital investment. Manufacturing fixed-capital investment represents the capital necessary for the installed process equipment with all auxiliaries that are needed for complete

process operation. Expenses for piping, instruments, insulation, foundations, and site preparation are typical examples of costs included in the manufacturing fixed-capital investment. Fixed capital required for construction overhead and for all plant components that are not directly related to the process operation is designated as the

nonmanufacturing fixed-capital investment. These plant components include the land, processing buildings, administrative, and other offices, warehouses, laboratories, transportation, shipping, and receiving facilities, utility and waste-disposal facilities, shops, and other permanent parts of the plant.

Working Capital Investment

The working capital for an industrial plant consists of the total amount of money invested in (1) raw materials and supplies carried in stock, (2) finished products in stock and semi-finished products in the process of being manufactured, (3) accounts receivable, (4) cash kept on hand for a monthly payment of operating expenses, such as salaries, wages, and raw-material purchases, (5) accounts payable, and (6) taxes payable.

The ratio of working capital to total capital investment varies with different companies, but most chemical plants use an initial working capital amounting to 10 to 20 per cent of the total capital investment.

Check Out: GATE Previous Year Cutoffs for All Branches

Methods of Cost Estimation

Methods of Cost Estimation play a critical role in various industries, including construction, manufacturing, and engineering. This study notes explore different approaches and techniques used to accurately assess and predict project costs, enabling effective financial planning and decision-making.

Cost Indexes

The method involving cost indexes is used for obtaining preliminary cost estimates by considering the historical data of similar past projects. Cost indexes (or indices) are dimensionless numerical values which represent the price change of individual or multiple cost items over time with respect to a reference year. Cost indexes are used to update the historical cost figures and to obtain the current cost estimates. The relationship used for updating the historical cost figures to the cost at another point in time using the cost index is presented below.

Or,

Where

Cn = estimated cost of the item in year ‘n’

Cr = cost of the item in year ‘r’ (at an earlier point of time and n > r )

I n = index value in year ‘n’

Ir = index value in year ‘r’

Here ‘r’ is the reference year (i.e. at an earlier point in time) at which the cost of the item is known and ‘n’ is the year for which the cost of the item is to be estimated. Cost indexes are periodically published by various public and private agencies.

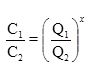

Estimating Equipment Costs by Scaling

Power-sizing model is most commonly used for obtaining preliminary cost estimates of industrial plants and equipment. The power sizing model relates the cost of a plant or system to its capacity or size and uses the following relationship for cost estimates.

Where

C1 = cost of Plant/equipment 1

C2 = cost of Plant/ equipment 2

Q1 = capacity or size of Plant/ equipment 1

Q2 = capacity or size of Plant/ equipment 2

x = power-sizing exponent or the cost-capacity exponent

One of the models is called the six-tenth (6/10) factor rule, according to this rule x =0.6

Unit-Cost Estimate

This technique is used for preparing preliminary estimates (i.e. order-of- magnitude type estimates). This estimate is generally prepared during the conceptual planning phase of a project, with less information available with the estimator. In this method, the total estimate of cost is limited to a single factor. Examples of some of the ‘per unit factor’ used in construction projects are construction cost per square meter, housing cost per border of a hostel, construction cost per bed for a hospital, maintenance cost per hour, fuel cost per kilometre, construction cost per kilometre for a highway etc. The total cost is calculated by multiplying the cost per unit factor by the number of units of the corresponding factor. For example, a preliminary estimate is required to estimate the cost of constructing a new reactor of 120 cubic meters. If the cost per cubic meter is Rs.10,000 (assumed), then the cost of constructing the house will be Rs.1200,000

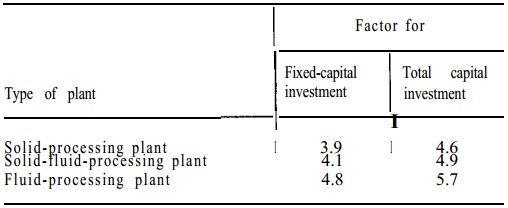

Lang Factors Method

This technique, proposed originally by Lang’ and used quite frequently to obtain order-of-magnitude cost estimates, recognizes that the cost of a process plant may be obtained by multiplying the basic equipment cost by some factor to approximate the capital investment. These factors vary depending upon the type of process plant being considered. The percentages given in Table 1 are rough approximations which hold for the types of process plants indicated.

Table 1: Lang multiplication factors for the estimation of fixed-capital investment or total capital investment

Factor x delivered-equipment cost = fixed-capital investment or total capital investment for major additions to an existing plant.

Get complete information about the GATE exam pattern, cut-off, and all those related things on the BYJU’S Exam Prep official youtube channel.